Massachusetts Housing Market 2026: What Rising Inventory and Price Adjustments Mean for Buyers and Sellers

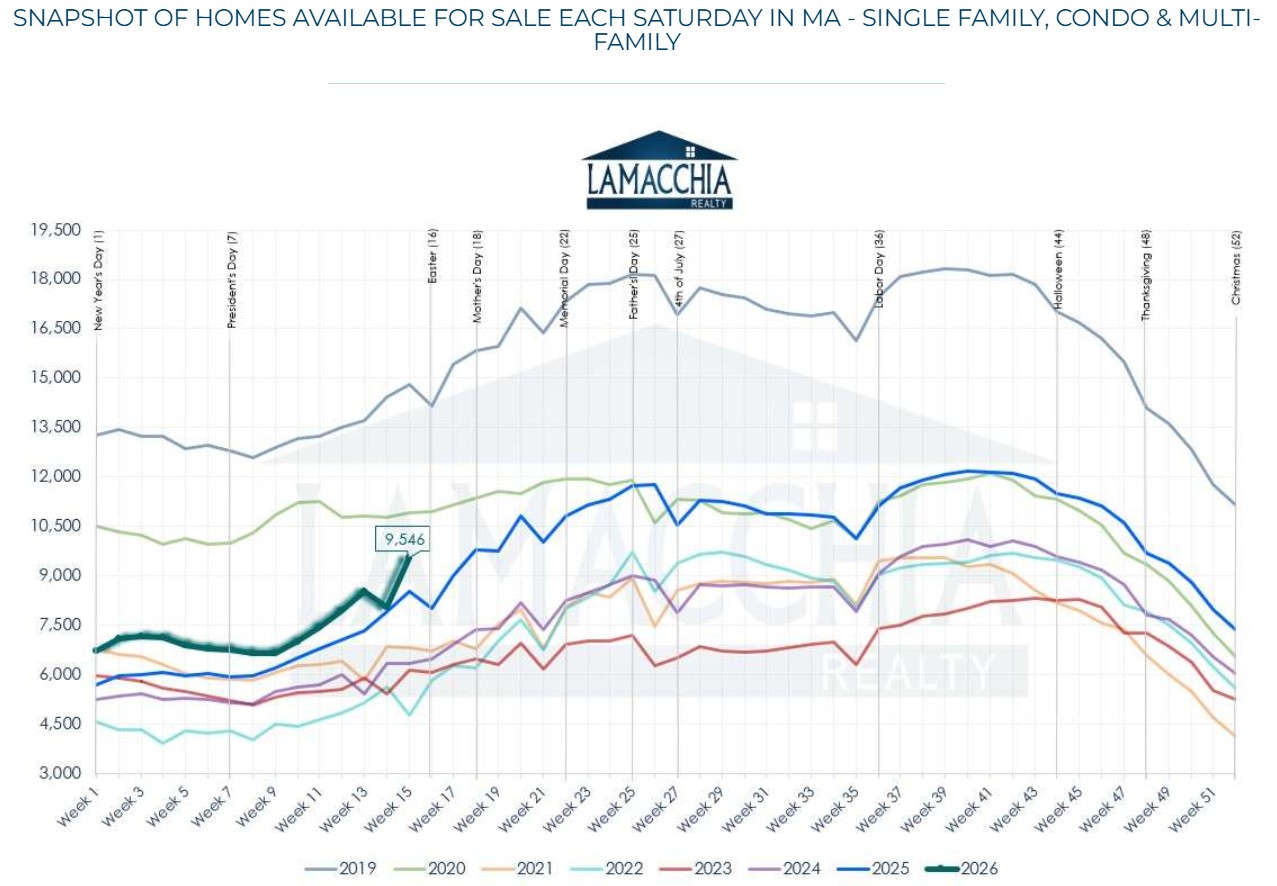

Massachusetts just crossed a threshold much earlier than last year: active home inventory has surpassed 10,000 listings. That single data point quietly signals a major shift in who holds power in the Commonwealth's real estate market. For buyers who've spent years being outbid, waiving contingencies, and paying over asking, this is the opening they've been waiting for. For sellers, it's a wake-up call that the rules have changed.Anthony Lamacchia, Owner and Founder of Lamacchia Realty, has been watching this shift closely. In his 2026 market predictions released at the end of 2025, he called 2025 "the pivot year where the real estate market began to head back in the right direction" — and everything unfolding in the Massachusetts housing market in 2026 is bearing that out.And the most visible symptom of that change? Price adjustments.

How We Got Here

For most of the past six years, Massachusetts sellers operated with a near-unfair advantage. Inventory was so tight that homes routinely attracted multiple offers within days of listing, bidding wars pushed prices well above ask, and buyers desperate to compete sometimes waived inspections entirely. According to Lamacchia Realty, the state began 2025 with just 5,928 homes on the market in mid-January — a number that nearly doubled to almost 11,000 by late spring, and ultimately climbed to just over 12,000 by fall 2025, the highest level since 2019.

Now, heading into spring 2026, that momentum has carried forward. The Massachusetts Association of REALTORS® reported in April 2026 that new condo listings jumped 17.2% year-over-year in March, while single-family new listings were up 1%. Banker & Tradesman noted that statewide active listings recently stood at approximately 10,600 — roughly 6% more homes for sale in Massachusetts than at the same point last year.

That number matters enormously, because inventory is the single most powerful lever in housing pricing.

The Historical Precedent Is Stark

Lamacchia Realty's long-view data offers a sobering historical parallel. In 2005, Massachusetts had just over 20,000 homes for sale. By 2006, that figure had surged to over 34,000. Prices began falling within a year. Then from 2010 onward, inventory gradually declined, demand grew, and prices climbed steadily for over a decade.

We're now in the early stages of the reverse cycle — inventory rising, buyer competition easing, and the pricing dynamic tipping from a seller's market toward a more balanced one. The critical difference from 2008, as experts are careful to point out, is that this is not a crash scenario. Homeowners today carry substantial equity, lending standards are far tighter, and many locked in sub-3% mortgages they've been reluctant to trade away.

Lamacchia's outlook for the Massachusetts housing market in 2026 is cautiously optimistic, not alarming. He is confidently predicting sales will be up at least 10% across Massachusetts and the broader New England market, and forecasts a 4% increase in average home prices — growth that is real but measured. "Supply will still be lower than demand for most of the year," he has noted, "so prices will continue to rise, albeit at a more measured pace. That added inventory will keep somewhat of a cap on prices and prevent them from rising too much." That framing aligns precisely with what the data is showing: this is a recalibration, not a collapse.

But make no mistake: sellers no longer control the room.

Massachusetts Price Adjustments Are Already Happening — and Will Accelerate

The data tells a clear story — and it's moving fast.

In Massachusetts, Houzeo's current market analysis shows that the share of homes with price reductions has climbed from 39.81% to 50% year-over-year — a striking jump that would have been unthinkable during the pandemic bidding-war years. At the same time, the share of homes selling above asking price has dropped from 33.98% to just 23.68%, and the sale-to-list ratio has fallen 4.32% annually. As recently as November 2025, roughly 41% of Massachusetts homes were still selling above list price while about 46% sold below asking — a market straddling the fence between seller's market and buyer's market. Now, that balance has tipped noticeably toward buyers.

Nationally, the signals are equally unmistakable. HousingWire data for the week ending April 3, 2026 showed that 34.44% of all single-family listings had experienced price cuts. ResiClub's analysis found that roughly 33% of the nation's 300 largest housing markets were registering year-over-year price declines as of early 2026 — up sharply from just 10% of markets at the same point in 2025. Even new construction isn't immune: the NAHB reported that 36% of builders cut prices in April 2026, with an average reduction of 5%, and for 13 consecutive months more than 60% of builders have been offering sales incentives to move homes.

In Massachusetts specifically, the picture is more nuanced than the national softening: the state still posts one of the strongest absorption rates in the country at 19% weekly, but closed sales dipped 2.2% year-over-year for single-family homes in March and 1.3% for condos, per MAR. What that combination tells us is a market in transition: homes that are priced correctly still move quickly, but overpriced listings are sitting — and sitting listings eventually lead to reductions.

In the multifamily segment, MLS Property Information Network data through early 2026 found that over 720 listings across the state saw price adjustments over a six-month window, with an average reduction of approximately 6.3% per property. Higher-end listings above $1 million saw steeper cuts of 6.6% to 10.8%.

Critically, the Massachusetts price adjustment story is fundamentally different from what's happening in the Sun Belt. ResiClub notes that the markets seeing the most softness nationally are concentrated in Gulf Coast and Mountain West regions — places like Tampa and Austin that saw outsized pandemic-era price surges, now grappling with a glut of new construction and prices that outran local incomes. Massachusetts has none of those conditions. Price reductions here are a function of individual sellers overpricing in a shifting market — not systemic weakness. That distinction matters enormously for anyone trying to read the tea leaves.

For sellers who became accustomed to listing high and watching a bidding war fill the gap — that strategy is fading.

What Drives a Seller to Cut the Price?

Lamacchia Realty's "target pricing model," developed back in 2006 and refined through multiple market cycles, offers a practical diagnostic for Massachusetts home sellers:

Getting showings but no offers? A 3–5% adjustment is typically warranted.

Sparse showings, only a few drive-bys? Expect to need a 6–11% reduction to reset buyer interest.

No showings at all? At least a 12% cut is likely required to get back into the market's active conversation.

These aren't arbitrary guidelines — they reflect buyer psychology in a more balanced market. When inventory expands, buyers have options. A home priced at the high end of its comparable range no longer carries the fear-of-missing-out urgency that drove overbidding. Instead, buyers compare, deliberate, and increasingly invoke their negotiating leverage.

Trelora reported in early 2026 that roughly 44% of home sales now involve some form of seller concession — whether that's closing cost contributions, price reductions, or rate buydowns — compared to the frenzied early 2020s when sellers routinely demanded cash-only, waived-inspection offers.

The Rate-Lock Thaw: A Market-Changing Shift

One of the most significant — and underappreciated — forces that could accelerate inventory growth in the Massachusetts housing market in 2026 is the gradual unwinding of the mortgage rate lock-in effect.

For the past several years, millions of homeowners who secured sub-3% and sub-4% mortgages during the 2020–2022 pandemic boom had little financial incentive to sell. Trading a 2.75% mortgage for a 7%+ rate meant a dramatically higher monthly payment, often for a similar or smaller home. The math simply didn't work for many who might otherwise have listed.

But that calculus is shifting meaningfully. Wolf Street's updated tracking of Federal Housing Finance Agency data puts the share of homeowners with a mortgage rate below 4% at approximately 50.6% — down from a peak of roughly 65% in early 2022, and falling every quarter as mortgages are paid off or retired through home sales. For context, Reventure App analysis notes that by early 2026, the share of homeowners with a rate above 6% has likely surpassed the share still holding sub-3% mortgages — a symbolic but meaningful crossover that signals just how much the market's rate composition has shifted.

The psychological shift is just as important as the financial one. When rates were touching 7.5–8% in 2023, giving up a 3.5% mortgage felt almost irrational. But with 30-year fixed rates now averaging 6.37% as of early April 2026 — down from 6.62% a year ago — the gap between a homeowner's existing rate and today's prevailing rate has narrowed considerably. Moving from a 4% mortgage to 6.37% is a real cost, but it's a far more manageable leap than moving from 3% to 7.5%. For Massachusetts sellers who've been sitting on the fence, that difference may finally tip the decision.

As the National Mortgage Professional noted, life events — new jobs, growing families, retirement downsizing — are increasingly outweighing the financial benefit of clinging to a rock-bottom rate. The lock-in effect is easing, and each quarter that passes shrinks the pool of homeowners for whom selling feels financially prohibitive.

This is precisely why we anticipate that the combination of rising inventory and more tolerable mortgage rates will encourage sellers who have been on the sidelines to finally enter the 2026 market. The "golden handcuffs" aren't fully off, but they're looser than they've been at any point since 2022. Lamacchia has said he suspects mortgage rates will settle in the mid to low-5% range by the end of 2026 — and that if that happens, "the golden handcuffs of those pandemic-era mortgage rates will really begin to open and create more home seller activity in the market, providing more selection for buyers." The Mortgage Bankers Association forecasts rates will hold in the 6.1–6.3% range through 2026 — meaning even without hitting the low-5% threshold, the trend is already moving in a direction that is unlocking seller activity.

A Market Divided: Single-Family vs. Condos

Not all property types are moving through this transition equally. The condo market is softening faster and more visibly. MAR data for March 2026 showed the median condo sale price actually declined 1.5% year-over-year, while single-family homes still showed a 4.4% gain. As one Boston real estate team put it, buyers looking for single-family properties still face real competition, but the condo market has measurably more breathing room.

This split will likely intensify through mid-2026 as continued inventory growth hits the condo segment disproportionately. Buyers who can stretch to single-family will likely continue to compete; buyers in the condo range increasingly have leverage.

Regional Variation Is Everything

Statewide averages can obscure dramatic local differences across the Massachusetts real estate market. Boston's absorption rate of 21.4% per HousingWire is one of the highest in the country, and the Boston metro median has exceeded $1 million. Worcester remains highly competitive, ranking among the top markets nationally for home sales growth. In contrast, suburban and secondary markets are showing more breathing room, and the Cape Cod and vacation home segment continues to attract steady out-of-state demand largely insulated from rate-lock pressures. JVM Lending's 2026 forecast projects statewide appreciation of 3–5%, with Boston and Cambridge at the upper end and Western Massachusetts closer to 2–3%.

What This Means for Buyers in 2026

This is the most favorable entry window Massachusetts buyers have seen in roughly five years — but "favorable" is relative. Prices aren't dropping; they're moderating. What buyers are gaining is:

More time to decide. Fewer bidding wars mean buyers can conduct inspections and negotiate. Trelora notes that fewer than 18% of buyers are now waiving inspections, down dramatically from the pandemic frenzy.

Concession leverage. With 44% of deals involving seller concessions nationally, requesting seller-paid rate buydowns or closing cost credits is increasingly normalized — and worth building into any offer strategy.

Price bracket opportunities. When overpriced listings are reduced to the next bracket (e.g., from $475,000 to $449,000), they surface to a new pool of buyers who should be ready to move quickly on attractively reset properties.

When to Sell a House in Massachusetts in 2026

The fundamental advice from every corner of the Massachusetts real estate market update is the same: price accurately from day one.

Lamacchia Realty puts it plainly: homes that sell fast sell for more money. Delayed price adjustments don't just cost time — they cost money, because the longer a listing sits, the more buyer skepticism accumulates. The Massachusetts 2025 Year in Review from Lamacchia Realty noted that the number of price changes statewide increased by 27.4% in 2025 compared to 2024 — a sign that sellers are already learning to meet buyers where they are, rather than where they wish the market still was.

For sellers who have been waiting on the sidelines, the window is genuinely opening. As Lamacchia noted in his 2026 predictions, more homeowners who are "want-to-be sellers" are coming off the sidelines — and crucially, many of those sellers will also be buyers, creating the kind of move-up activity that has been largely absent from the Massachusetts market for three-plus years. The rate environment is more hospitable than it's been since 2022, inventory is rising to give you better odds of finding your next home, and buyer demand — while moderated — remains real. As Banker & Tradesman noted, years of price appreciation have put many Massachusetts homeowners in a strong equity position to make the move, regardless of rate concerns.